The U.S economy is grappling with historically high inflation rates–averaging 8.05% through the first four months of 2022, a rate not seen since 1981. Not surprisingly, curbing inflation has become front and center for the Fed with a telegraphed plan to hike the Fed Funds rate 50 more basis points this year, not including its most recent half percentage point increase. April’s interest rate hike was also significant in that it was the largest single increase in over a decade. Needless to say, the Fed is concerned about inflation.

And while everyone’s eyes are on each month's inflation numbers and on the volatility in the stock market, GDP also dipped in Q1 by 1.4% on an annual basis, pumping even more panic in the headlines.

So what caused this GDP dip and should we panic? The short answer is, “we don’t believe so,” but let’s unpack that statement.

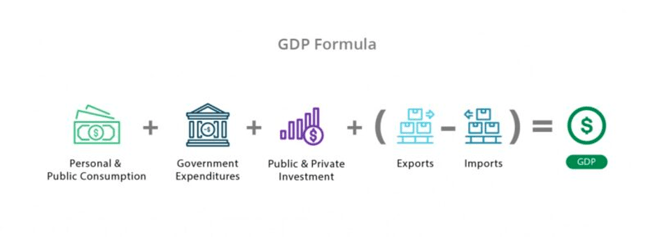

Figure 1: What is GDP made up of?

The Gross Domestic Product is a quantitative measure of how much an economy produces. It includes the monetary value of both goods and services within a specific nation's borders.

Source: GDP, Investing Answers

The GDP equation, much like the economy, is like a machine. If one part is not functioning well it can hinder the entire output. When breaking down the equation today, it’s clear that some parts are functioning well while others are not. Let’s dive into both the major positive and negative contributors to the GDP.

Figure 2: Contributors to the Q1 2021 GDP

| Contributors to the U.S. GDP |

Annual Percent Change Q1 2022 |

| Personal consumption expenditures |

+1.83 |

| Goods |

-0.03 |

| Services |

+1.86 |

| Gross private domestic investment |

+0.43 |

| Fixed Investment |

+1.27 |

| Change in Private Inventories |

-0.84 |

| Net exports of goods and services |

-3.20 |

| Exports |

-0.68 |

| Imports |

-2.53 |

| Government consumption expenditures and gross investment |

-0.48 |

| Federal |

-0.39 |

| State and local |

-0.08 |

| Gross Domestic Product (GDP) Q1 2022 |

-1.4% |

Source: Condensed version of Table 2 “Contributions to Percent Change in Real Gross Domestic Product”, Bureau of Economic Analysis.

Negative Contributors

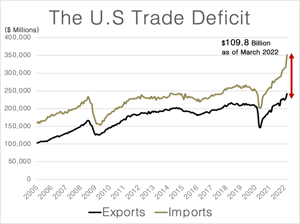

Imports increased significantly more than exports

The main contributor to the negative GDP growth came from an increase in imports, a subtraction from the GDP equation. The U.S is the second-largest importer in the world and many of our local needs, including crude oil and consumer goods, are increasingly being met by imports. And because exports did not increase by a similar amount, this further increased the gap between exports and imports, pushing the U.S trade deficit to historically high levels.

With the dollar becoming more expensive, the trade deficit is expected to increase as it is becoming more expensive for foreign countries to afford U.S products and services, which may further limit exports.

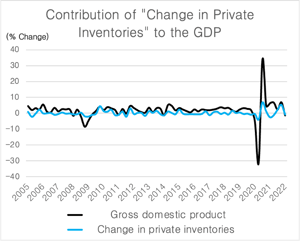

Business inventory investment reduced due to overstock

The second major contributor which led to a decrease in the GDP was the “change in private inventories,” or CIPI, which is essentially the change in the physical volume of inventories owned by private businesses from one period to another. Note that when businesses' inventory investment is stronger than usual during one period, it is usually followed by a slow down of inventory investment in the following period because businesses are satiated and can only hold so much on their shelves before it starts to burden their balance sheet. Essentially, the higher-than-expected inventory investment in Q4 2021 led to a negative CIPI or negative change in inventories for Q1 2021, contributing negatively to the GDP.

| Figure 3: The U.S. Trade Deficit | Figure 4: Change in Private Inventories |

|

|

Source: Bureau of Economic Analysis

It is important to note that although an important metric, CIPI is considered one of the most volatile pieces of the GDP and is used mainly to determine short-term variations in the overall GDP growth. Keeping in mind that the supply chains are still distressed, we expect more volatility in the trade and CIPI parts of the GDP equation.

The government reduced its spending

Both federal, state, and local government spending trailed down which pulled the GDP down. The major pull came from reduced spending on defense purchases.

Positive Contributors

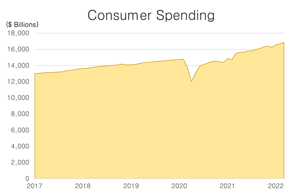

Personal consumption expenditures went up

Spending on goods and services is often considered the economic engine for employment, and it is the largest contributor to GDP growth. Consumer spending went up by 2.7% annually with a retraction in the unemployment rate which is currently hovering at 3.6%, down significantly from its pandemic high of 14.7%. The consistent rise in consumer spending is a bit surprising, especially with inflation at record levels and consumer confidence at a decade low.

|

|

Source (left): Bureau of Economic Analysis Source (right): Collision Week

Increased fixed investment

Fixed investments include both residential and non-residential components like business equipment and intellectual property. A private investment is “fixed” when you hold that asset for more than a year and cannot use the capital that is invested. Fixed investments can give clues about the economy's capacity to produce more by answering the question, “Are businesses spending enough on new fixed assets to replace old ones?” With that in mind, an increase in fixed investment is a healthy indicator of current and future business productivity.

Fun fact: Did you know that the music industry contributed about 0.9% to the total GDP in 2018? Songs are intellectual property and the creation of songs is considered a fixed investment that contributes to the GDP.

The million-dollar question remains–are we headed toward a recession?

Possibly, but more importantly, it depends on how one defines a recession. It is commonly and historically believed that a recession is two consecutive quarters of declining GDP. However, the National Bureau of Economic Research (NBER), which officially declares a recession in the economy, has a more nuanced definition. NBER defines a recession as a “significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.” And with volatility in some of the GDP metrics, especially due to supply-chain distress and the trade deficit, it would be myopic to automatically declare a recession following two volatile periods of negative GDP (were that to happen) assuming consumer spending and business investment remain strong.

With expected volatility in the supply chains and business inventories, another metric we can observe to take the pulse of the economy is called the “real final sales to domestic purchasers'' which is essentially the GDP calculation, but without the change in inventories, government spending, and net exports. While the GDP dipped, real final sales increased by 3.7% in the first quarter of 2022 on an annualized basis showing strong private sector demand with increased business investment and consumer spending.

However, the fears of a recession have plunged consumer confidence to decade lows despite signs of strength in the U.S economy. At the end of the day, real wage increases paired with productivity, low unemployment rates, increase in consumer spending, healthy supply chains, and, most of all, reasonable inflation rates are all needed to return the economy to more normal conditions. The significant and record-breaking price appreciation of both residential and commercial real estate in the last few months alone, paired with a rapid jump in the inflation rate, is an unsustainable dynamic that is already starting to change. The latest Greenstreet CPPI index showed price appreciation went up by only 0.2% quarterly compared to a whopping 21% annual increase in 2021. We expect the same with housing prices as interest rates bring demand back to more sustainable levels.

Treasury Secretary Janet Yellen, was recently interviewed byThe Wall Street Journal and explained that the Fed will try its best to achieve a “soft landing” and that the economy is overall strong despite the high inflation which is top priority to bring down.

“I’m certain that the Fed will try to deploy its tools to achieve a soft landing where the economy can continue to grow, we avoid a recession, but inflation comes down. I’ve said before that the Fed will need to be both skillful and lucky to achieve that but I believe that it's a combination that is possible in part because although inflation has been very high and that has taken a real toll on households and really needs to end, I don’t think it’s deeply ingrained in the U.S economy," Yellen said.

She also went ahead to explain that credit quality is “excellent” and banks are well-capitalized. In a statement from Benjamin Harris, the Assistant Secretary for Economy Policy, the GDP outlook is estimated to grow at 2.3 percent over the next four quarters. “Although this estimate may be revised down—and downside risks remain to the outlook—the U.S. economy is expected to continue its expansion this year. Waning fiscal and monetary stimulus along with recovering labor supply should help balance labor markets and relieve some inflationary pressures,” the statement read.

On the other hand, an analysis by VoxEu points to the fact that a soft landing might not be possible. Historical evidence suggests that “there has never been a quarter with average inflation above 4% and unemployment below 5% that was not followed by a recession within the next two years.” With unemployment currently at 3.6% and inflation rates at 8.6%, past predictors could play out again in the future. However, the COVID-19 pandemic was unprecedented and brought unique challenges and eventual recovery to the state of the economy. It’s fair to expect a unique recovery this time around but supply chains will need to recover to match demand and, correspondingly, inflation will need to come back to reasonable levels.

When placed into a broader context, the negative GDP growth in Q1 begins to look a lot like a correction from Q4 2021. Things are rarely as good or as bad as they seem in the heat of the moment. In retrospect, it now appears that Q4 2021 GDP growth was not actually as robust as the 6.9% annualized rate of growth reported by the Bureau of Economic Analysis and much of what transpired in Q1 2022 served as an adjustment to previously overstated growth. Q1 2022 also reminds us that it is important to parse through multiple layers of macroeconomic indicators to determine the overall health of the economy. Observing a complex machine like the economy with a one-size-fits-all lens can be deceiving if not properly interpreted or understood. The economy is undeniably in a turbulent state but there’s enough underlying strength in multiple fundamentals to suggest that, even if we enter into recession, it may be brief in duration and mild in depth. However, some of that outlook will depend on our supply chain ramping up in the coming quarters to meet demand and bring inflation back below 4% by next year.

As the situation unfolds, we will continue to provide our analysis and insights to investors. For further reading, please check out our 2020 analysis on “How Commercial Real Estate Investors Survived the Last Recession” to equip your mindset with ways to navigate a recession.