Written by Zachary Frey

A Three-Year Journey of Economic Shifts Leads to Potential Trough

What happens when you inject trillions of dollars into a relatively healthy economy while simultaneously shutting down global supply pipelines? Over the past three years, we have learned the answer: rapid inflation, followed by one of the most abrupt rate hike cycles in U.S. history. The culmination of these events led to historic levels of macroeconomic market volatility.

Today equity markets are hitting all-time highs, while the less agile and illiquid commercial real estate (CRE) market finds itself in search of its trough. Concurrently, signs point to large institutional investors looking to deploy dry powder amounting to hundreds of billions of dollars in 2024 and 2025, potentially indicating that the current market dislocation may be brief and we could be close to reaching the trough for CRE.

All this is to say that within the financial sector, the flow of capital is generally considered a crucial indicator of demand, with the potential to influence everything from bond prices to stock surges. Typically, as demand for an asset grows, so does its price, oftentimes fueled by the influx of capital.

With this concept in mind, we are going to 'follow the money' as we explore the impact of the previous three years' capital flows and where commercial real estate stands today.

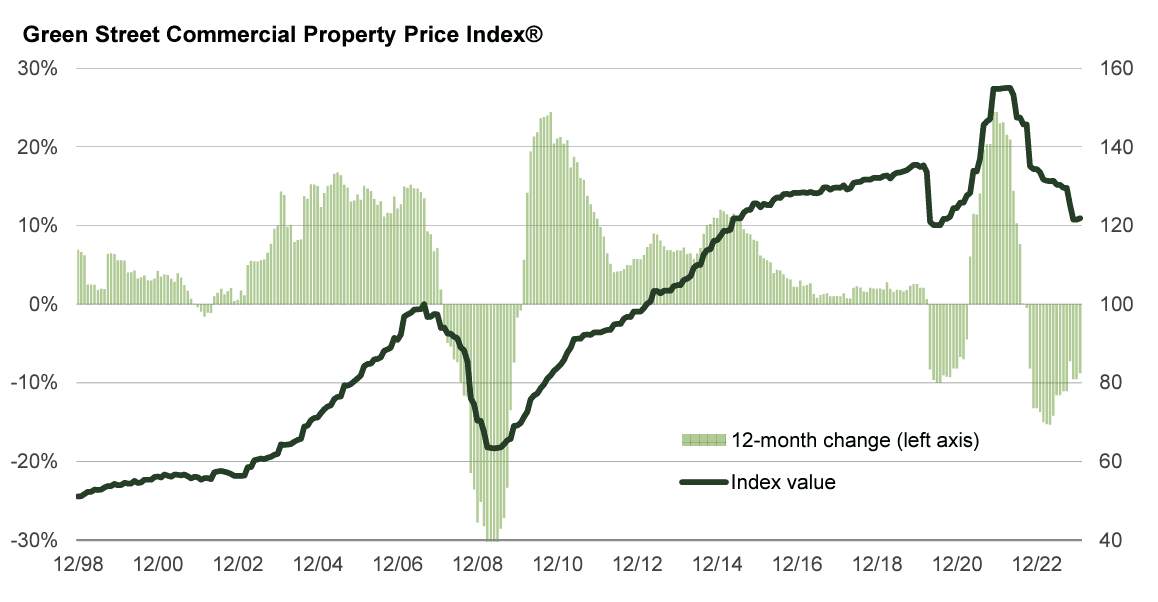

Figure 1: Green Street Commercial Property Price Index

The index value is based on property portfolios owned by U.S. REITs. It is driven by the NAV models of these REITs, which largely consist of stabilized, large market cap commercial real estate.

Source: Commercial Property Price Index, Green Street, February 2024.

How it Started: The Initial Impact of the Pandemic on CRE

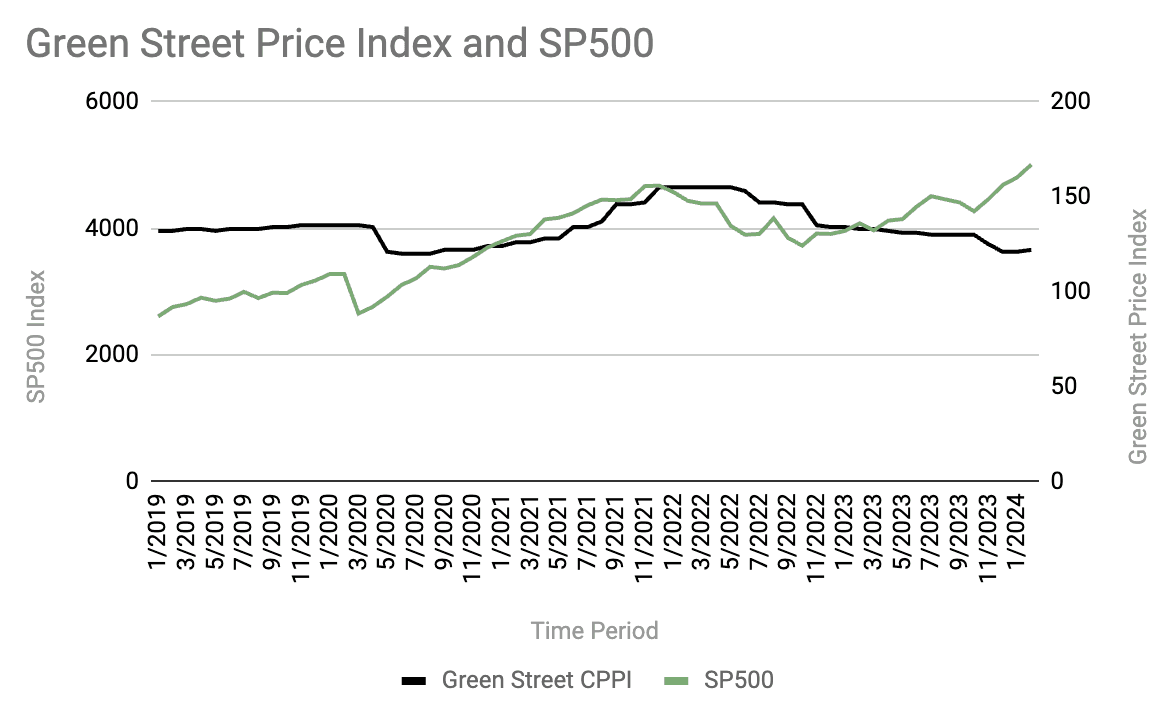

At the onset of the pandemic in 2020, CRE experienced a significant pullback, similar to the 19.9% decline in U.S. equities. The net asset value (NAV) of real estate investment trusts (REITs) declined across the U.S. commercial real estate market (Figure 1). As the chart below depicts, markets reversed quickly and CRE mirrored the gains of the equity markets through the first half of 2022. Both the commercial real estate and equities markets saw an appreciation in value, which we believe to be largely attributed to the 'wealth effect,' with many consumers and businesses finding themselves with an excess of cash and CRE market participants benefiting from the low-interest rate environment. Money was relatively abundant, credit markets were generally active, and, as we see from GreenStreet's index, CRE valuations climbed.

Figure 2: S&P 500 VS. Green Street Commercial Property Price Index

Source: S&P Dow Jones Indices & Commercial Property Price Index, Green Street, February 2024.

Then the Music (Money) Stopped

In March of 2022, the Federal Reserve announced the first of what would be an unprecedented 11 rate hikes over 16 months. This move had a significant impact on CRE, altering the dynamics of the sector. According to CBRE, 'Econometric evidence suggests that every 100-basis-point increase in long-term interest rates results in a 60-basis-point rise in commercial real estate capitalization rates.' Typically, when long-term rates rise, so do capitalization rates and when capitalization rates rise, values typically fall.

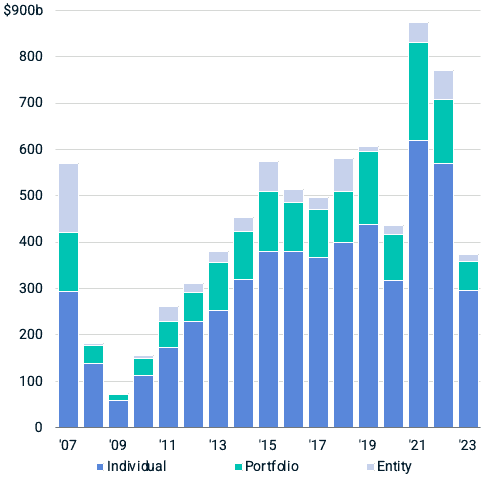

We see this phenomenon begin to unfold starting in the second quarter of 2022, with many market participants reversing course and pulling out of the market. Transaction volumes dropped significantly, as seen in the chart below.

Figure 3: Commercial Real Estate Annual Transaction Volume ($ Billion)

Source: US Big Picture, Capital Trends, MSCI Real Capital Analytics, 2023.

Debt Participants: The Exodus of Banks and Institutional Lenders

Entering the second half of 2022, banks and institutional lenders were among the first to retract within the capital markets. Many had large interest rate exposure with their Treasury positions, coupled with exposure to the general CRE market, particularly the rapidly deteriorating office market, which was expected to witness interest rate-induced distress. In the spring of 2023, the U.S. experienced a regional bank crisis tied to these exposures. At the time, commercial real estate represented 28.7% of regional banks' portfolios, according to Business Insider. The CRE credit markets dried up and, with less competition, the amount of capital for lending was substantially reduced and the cost of borrowing (interest rates) meaningfully increased.

Equity Participants: Stagnation in CRE Markets

The U.S. CRE markets experienced a significant slowdown in transactions, however, the debt market pullback is only a portion of the story. On the equity side of the equation, a similar plot unfolded. As the yield on long-term debt facilities, specifically the 10-Year Treasury, climbed, so did the required yield-on-cost that commercial real estate limited partner equity providers needed to achieve to justify investing. Simply put, deals didn't pencil. Construction costs were still elevated due to soaring demand in 2021 and 2022 and lingering supply issues from the pandemic. At the same time, according to Greenstreet's Commercial Property Price Index1, valuations for existing assets were at an all time high. While fundamentals were still strong in sectors such as industrial and multifamily, we observed that recession fears gave many limited partner investors hesitancy to assume the continuation of this trend. Debt was expensive, construction costs high, valuations inflated, and the future uncertain, causing many equity investors to press pause.

Owner Participants: Managing in the Post 'Free-Money' Era

Owners, who generally saw their properties appreciate in value, driven in part by the low-interest rate environment over the past decade, were largely reluctant to face the realities of a post-free-money, higher interest rate era. Instead, many decided to manage their existing portfolio and, as industry experts coined, attempted to 'survive to 25.' These potential sellers sat on the sidelines and many worked with their lenders to extend or modify their existing loans. Lenders, who generally had little desire to foreclose, take control, and ultimately sell these assets in a down market, increased their efforts to accommodate owners and prevent losses.

The culmination of these decisions ultimately led to a material reduction in transactions - which are a crucial component for the functioning of the illiquid commercial real estate market. According to Real Capital Analytics (RCA) and Linneman Associates,2 'Inflation-adjusted (2022 dollars) transaction volume in U.S. commercial real estate fell sharply in the third quarter of 2023, to $88.7 billion, from $189.3 billion a year earlier. The high of $392.1 billion in commercial real estate sales volume was seen in the fourth quarter of 2021.' The flow of capital into CRE slowed and has not yet regained speed as of March 2024.

Where Are We Now? Assessing the Current Capital Market Landscape

Following the Fed's December 2023 guidance, there is a general consensus among market participants that we are at the peak of the interest rate cycle. We believe this consensus is a critical step in unlocking the CRE transaction market. With the newfound clarity coming from the Federal Reserve, some potential buyers are beginning to find increased confidence in their ability to accurately underwrite potential acquisitions.

In addition to the general consensus that rates have peaked, data from FRED's FOMC Summary of Economic Projections surrounding the Federal Funds Rate suggests that the Federal Open Market Committee projects the median Fed Funds rate to fall 250 bps by the end of 2026. Despite projected rate cuts, there are concerns of distress in the CRE sector due to upcoming loans coming due in the next few years. Roughly 20% of outstanding loans, or $929 Billion are coming due in 2024, according to Mortgage Bankers Association, which would be a 28% increase from the amount of loans that expired in 2023. According to Fitch Ratings, the delinquency rate of commercial mortgage loans is expected to reach 4.5% in 2024 and 4.9% in 2025, more than doubling the 2.25% rate in 2023. To help put this into perspective, in 2008-2010, the delinquency rate of commercial mortgage loans averaged 6.96%, according to the Board of Governors of the Federal Reserve System. The potential convergence of confident buyers, a high volume debt maturities for lenders, and rising delinquency rates for borrowers has the potential to stimulate increased transaction volume, providing price discovery across the sector.

What's Coming Next? Insights from Industry Leaders

While we believe the flow of capital has influenced much of the volatility we witnessed in the commercial real estate market, we may also gain insight for tomorrow from understanding where capital has positioned itself today. For that, we look to some of the largest players in the industry.

Blackstone's President, Jonathan Gray, described in his third-quarter earnings call a 'potential spending spree' as the real estate asset manager looks to capitalize on the current market conditions and deploy the roughly $66B of dry powder. Mr. Gray explained, 'Higher interest rates are impacting valuation multiples in the sector. This is also meaningfully reducing the new supply pipeline.' He goes on to say, 'Construction starts are falling sharply for virtually all types of real estate, including year-over-year declines of 30% to 70% for US apartment buildings, warehouses, and hotels.' Generally, we've seen that reduced construction starts like these have the potential to positively impact values longer term.

Blackstone isn't alone as far as their sentiment toward CRE in 2024. According to CoStar, Bruce Flatt, CEO of Brookfield Asset Management, one of the world's largest real estate owners, recently said that he expects 2024 to be one of the best in a while for real estate investment based on money flowing into his company's funds. A Wharton professor and fund manager, Peter Linneman, summarized in his recent Linneman Letter,^2^ 'Hundreds of billions of dollars of investable equity are already raised, and trillions of excess bank reserves exist (versus literally none in previous episodes). The money is there, but financial institutions are not lending. It just needs the herd to start moving to restore the willingness to act.'

What's the Significance of Following the Money?

We believe by analyzing the flow of capital, both in and out of the sector, over the past three years, we have made more sense of the price volatility witnessed in Greenstreet's Commercial Property Price Index. As the commercial real estate capital markets begin to show signs of engagement, we find the gradual cyclicality of the illiquid CRE market likely still searching for its trough. We believe the challenge in navigating market cycles lies in the uncertainty of identifying the bottom or trough while in the midst of it. Only in hindsight, once the cycle has concluded, does the clarity usually emerge.

While the future is unknown, what we do know is that money is generally the catalyst that moves markets. Industry leaders are armed with hundreds of billions of capital and have indicated their readiness to deploy it in 2024. We believe that the tides may be changing and that signs point to CRE markets being near to hitting if not in its trough. As this massive amount of capital flows back into this sector, this window of market dislocation has the potential to be short-lived.

In our 2024 U.S. Commercial Real Estate Investing Outlook, we discuss how re-priced opportunities relative to peak 2022 pricing in markets with strong fundamentals and generally favorable supply/demand dynamics may surface during this period. For continued learning on CRE market cycles and strategies for various stages, find more in-depth information in this article - The Four Phases of the Real Estate Cycle.

{{ This article was written by Zachary Frey, an employee of CrowdStreet, Inc. ('Crowd Street') and has been prepared solely for informational purposes. Nothing herein should be construed as an offer, recommendation, or solicitation to buy or sell any security or investment product issued by Crowd Street or otherwise. This article is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any investor. All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. All investors should consider such factors in consultation with a professional advisor of their choosing when deciding if an investment is appropriate. Crowd Street's review process of an issuer, deal, investment type or strategy, market, or other investment criteria should not be construed as a recommendation or a solicitation to buy. All investors should consider their individual factors in consultation with a professional advisor when deciding if an investment is appropriate. }}