Are the Headwinds Changing into Tailwinds?

Considerations for Investing in 2025

We’re heading into 2025 with renewed optimism.

The Fed’s rate cuts and shift to a neutral stance are typically positive signs for private markets that rely on debt financing.

Deal volumes are gradually rebounding1, but we expect activity in 2025 to remain uneven as the market continues to stabilize and grow.

The actions of industry leaders and first-movers may signal growing confidence in the broader market. Major players like Blackstone, KKR, and Brookfield made large investments in 2024.2

Blackstone spent $22 billion on CRE investments in 2024, nearly 2.5 times the previous year, a significant portion of which went into acquiring apartment communities.3 Likewise, KKR acquired 5,200 apartment units totaling $2.1 billion, calling 2024 a "sweet spot for real estate investments"4 and reorganizing its $157 billion real assets platform to target opportunities like logistics and data centers with plans to invest more in 2025.5 Brookfield also expanded and readjusted its CRE portfolio, focusing on office, industrial, and multifamily assets in North America and Europe.6

Here are four key facts that could set 2025 apart:

Many CRE Deals Are Available at Discounts

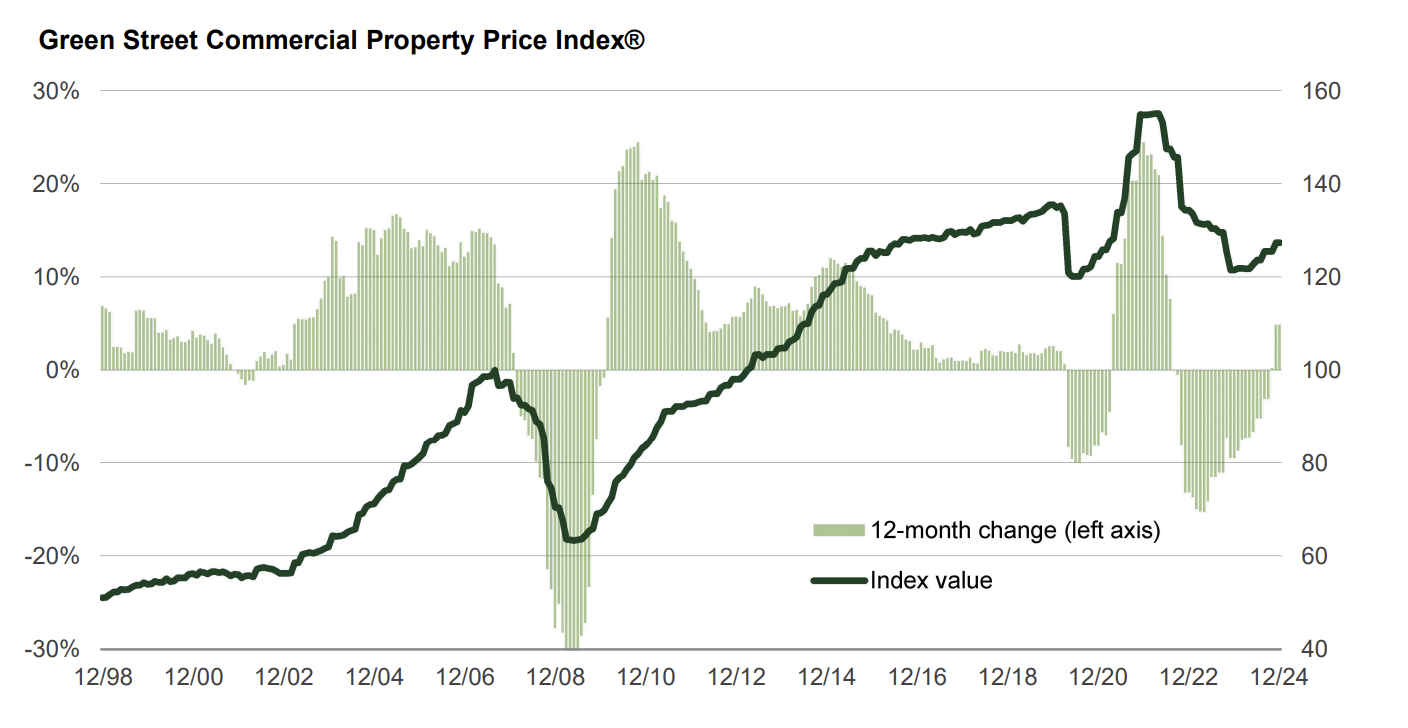

Prices immediately dropped when the Fed first raised rates in 2022 and then bottomed out around the end of 2023, declining by roughly 21% overall from their 2022 peak.7

In 2024, prices started increasing again, ending the year up 5%.7

Today, prices remain at discounts relative to 2022, ranging anywhere from 10% to upwards of 40%, depending on the type of CRE asset, according to the latest data shared by Green Street.7

This extended discount window is partly influenced by elevated Treasury yields8, which have a direct impact on capital flows and an indirect impact on capitalization (cap) rates and property values. Higher Treasury yields typically lead to capital outflows which can induce higher cap rates, resulting in lower property valuations. Conversely, declining Treasury yields can spur capital inflows, leading to cap rate compression and, potentially, increasing property values.

Barring any unforeseen economic shocks, we believe that 2025 may represent the tail end of a window to acquire discounted assets before prices rebound, especially if Treasury yields decline and the market stabilizes further.

Figure 1: Prices On The Rise Again: Property Values Up 5% in 2024

Source: Green Street Commercial Property Price Index, January 2025.

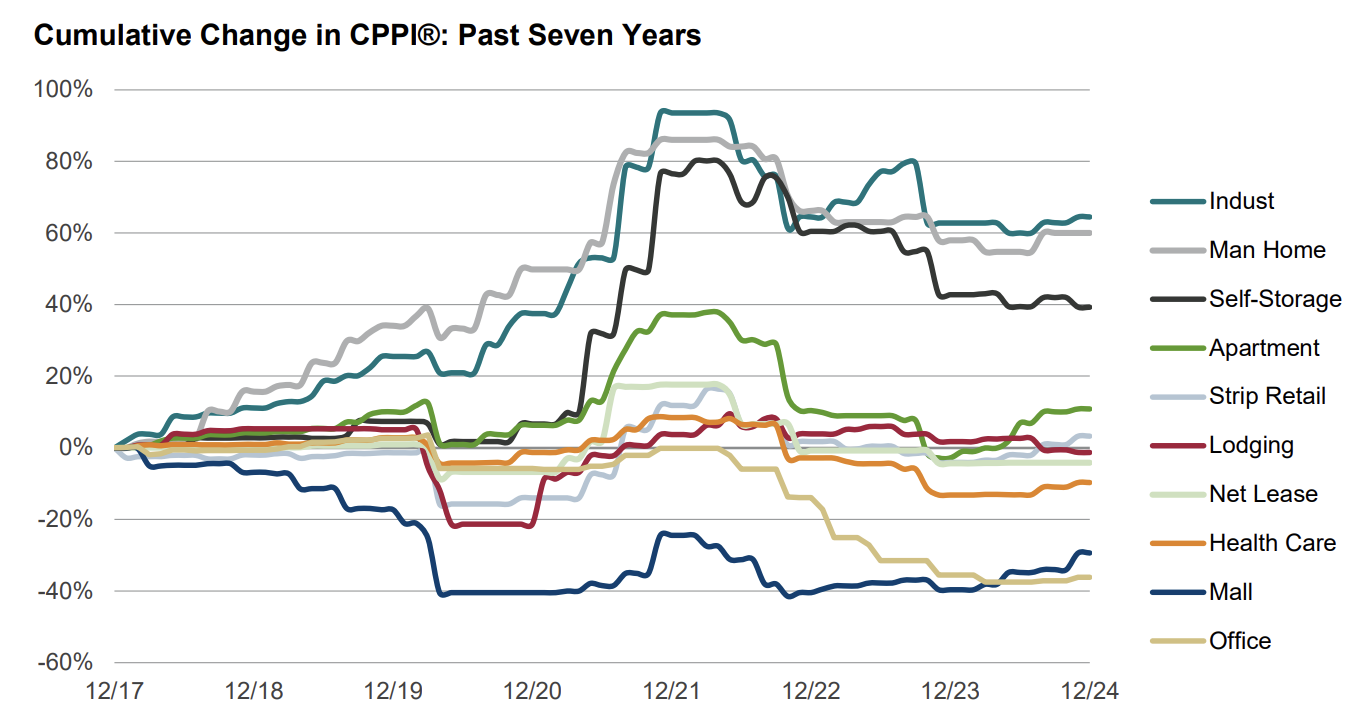

Figure 2: Steep Price Declines Have Mostly Stopped, Per Green Street

Source: Green Street Commercial Property Price Index, January 2025.

More Rate Cuts Expected

The Fed is taking a cautious approach to rate cuts as inflation stays stickier than expected. Still, most economists polled in early February expect two cuts in 2025, with the first likely by the end of June.

In the first meeting of the year, the Fed held rates steady, emphasizing a “wait and see” stance.10 Chair Powell noted that while the labor market remains strong and unemployment is stable, inflation is still somewhat elevated. He reiterated that the current policy remains “meaningfully above neutral” and that the Fed will likely need further confirmation of inflation tracking toward 2% before resuming cuts.10

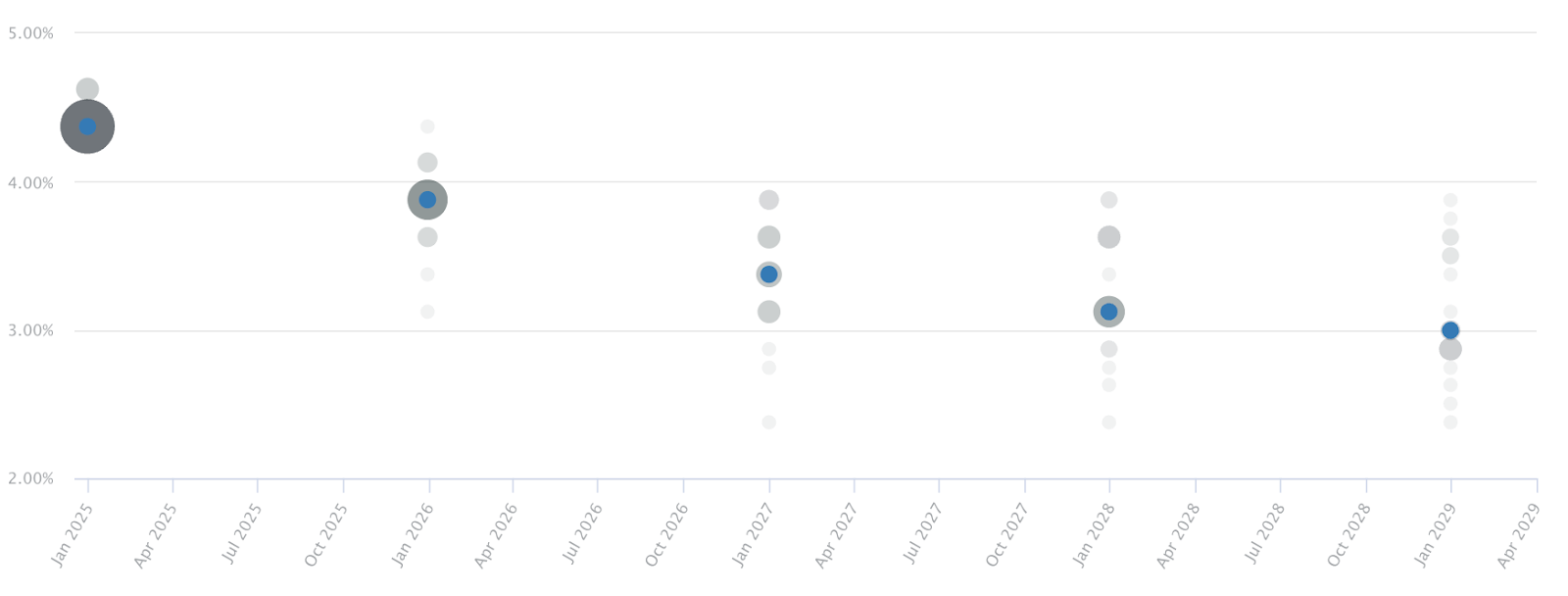

The chart below shows the Fed’s median projection for rates over the next few years. According to Chatham's forecast (as of 01/21/25), rates are expected to return to mid-2022 levels by the end of 2025, settling in the 3.75-4.0% range.11

Lower rates could improve lending conditions for private markets, potentially leading to further increases in property values and transaction volumes. But the new administration’s tariffs, along with other external factors, could affect the pace of rate cuts and broader market conditions.

Figure 3: Federal Reserve’s Rate Cutting Forecast, Per Chatham Financial

Source: Chatham Financial, January 21, 2025.

Broader CRE Market Fundamentals Are Stabilizing

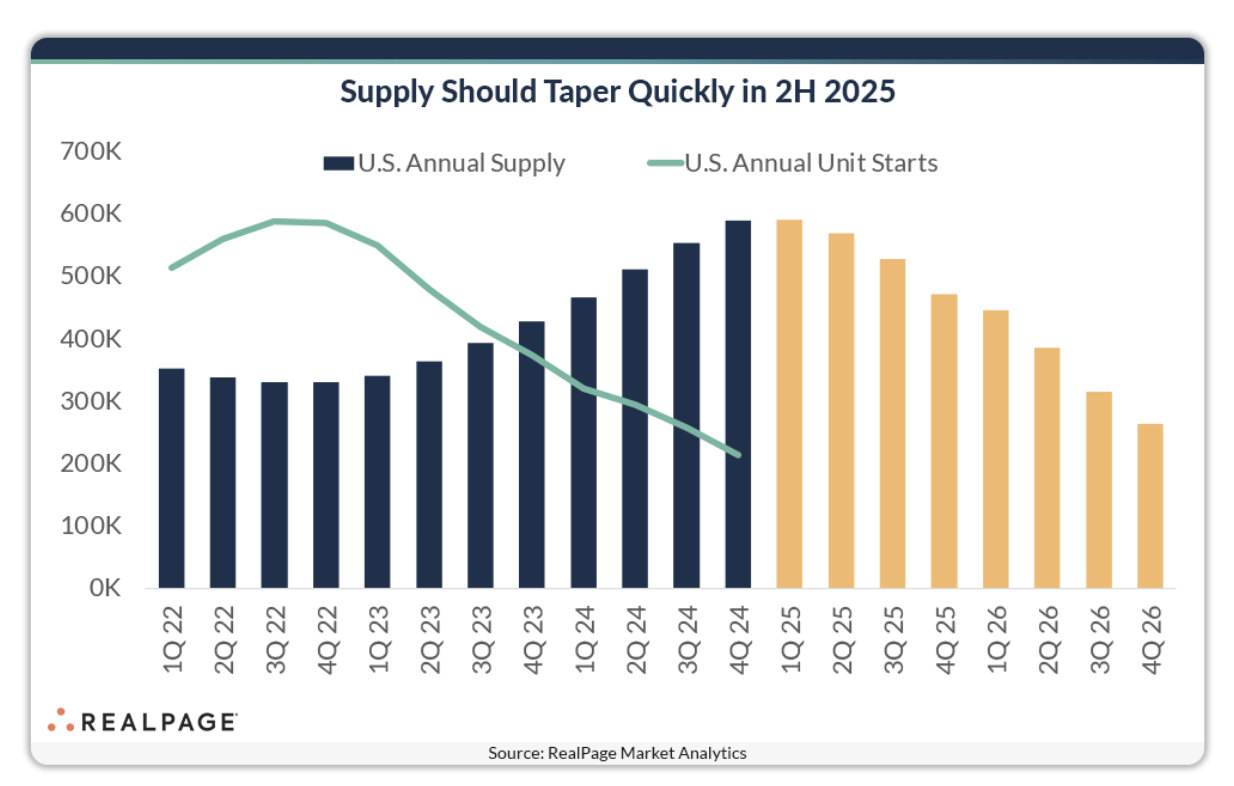

After the post-pandemic construction surge, supply levels spiked nationally, driven by record levels of construction in multifamily12 and industrial13 areas with strong population growth. This added pressure on rent growth and property valuations. While some markets still face oversupply, data shows steady absorption of that excess inventory, with multifamily breaking net absorption records in 2024.14

With new construction slowing, new supply is tapering, and rents in both the industrial and multifamily sectors are expected to see modest growth in 2025.15 This decrease in supply, paired with strong demand, may potentially create a favorable environment for rent increases in key markets, helping create an overall stronger supply-demand balance in 2025.

Figure 4: Apartment Supply Should Taper Quickly by H2 2025, Per Real Page

Source: Real Page, January 2025.

Challenges Remain

The combination of a rate-cutting cycle, tapering supply, growing rents, and discounted pricing on deals makes 2025 an interesting vintage to invest in. But while market conditions are generally improving, there are still hurdles to watch for that may affect deals:

- Overall, debt availability remains limited. Therefore, we expect growth in the number of investable opportunities to be slow, and financing to remain challenged.16

- Operational costs are still upsetting some projects. Overall costs to operate and build properties still remain high, with materials 40% higher than pre-pandemic levels.17

- Although generally, demand is catching up to supply, especially in the case of multifamily, some markets and property types may still be oversupplied in 2025.

- Lastly, the volatility of the 10-year Treasury yield isn’t yet supportive of market liquidity, which suggests that these broader market challenges may need to ease further before the market can fully recover and grow.8

Crowd Street’s focus in 2025: Quality.

The sponsors we intend to partner with will be cycle-tested with experience navigating both up and down markets. Our emphasis will be on well-capitalized, experienced sponsors with strong networks, as they might be better positioned to capitalize on unique opportunities and adapt to evolving market conditions.

Big Picture Outlook by Commercial Real Estate Asset Types

Multifamily Outlook

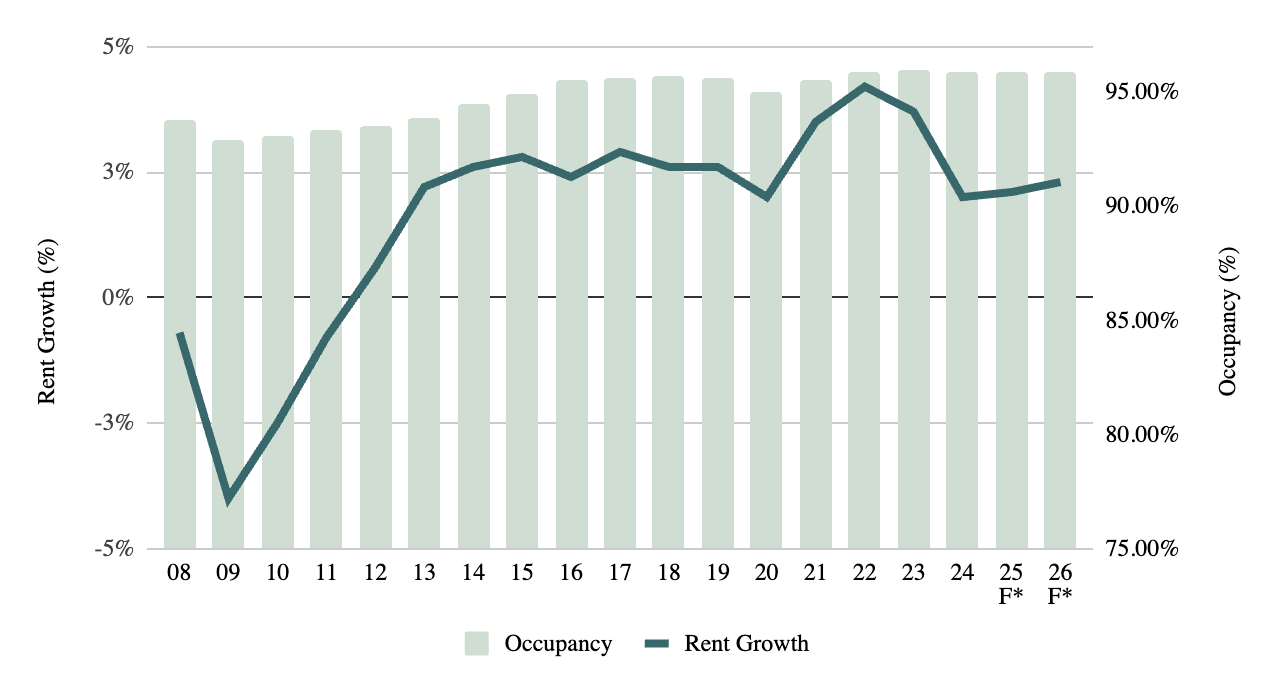

Multifamily demand is strong, with continued leasing growth in 2024.5 Rents are expected to grow in 2025; however, high costs, financing, and operational challenges may hinder growth.15

Many people are turning to rent due to the rising cost of homeownership, which is helping increase demand for multifamily housing. According to Bankrate, the cost of owning a home is at least 1.5x higher than renting today, pricing many out of the housing market.18

The sector is beginning to recover from the oversupply that emerged from the 2021 construction boom.15 Per CoStar, close to 535,000 more units were leased in 2024 compared to 2023 (data as of 12/13/24), marking the highest increase since 2021 recorded by CoStar.15 New York, Austin, Dallas, and Houston were the leading markets in this trend for 2024.15 With fewer empty units, CoStar projects rents will rise further in 2025, especially in mid-priced and more affordable segments.15 The Midwest and Northeast, which avoided the oversupply challenges seen in the Sun Belt, are seeing stronger rent growth. Meanwhile, new construction is expected to slow, with 2025 completions forecasted to drop by roughly half compared to 2024, per CoStar. This is likely to boost occupancy rates and rents.15

Despite improving fundamentals, the sector faces ongoing financing and operational challenges. Trepp data shows over $96 billion in loans are at risk of refinancing issues due to high borrowing costs.19 Driven by jumps in the cost of labor, materials, maintenance, and insurance, the average expense per unit rose 27.4 percent in the four years ending August 2024, per Yardi Matrix.19 These pressures are expected to persist, which could make sustained growth more challenging.

Figure 5: Multifamily Market Fundamentals by Year with Forecast Per CoStar

Source: Multifamily, CoStar, December 2024. *F stands for Forecast per CoStar.

Industrial Outlook

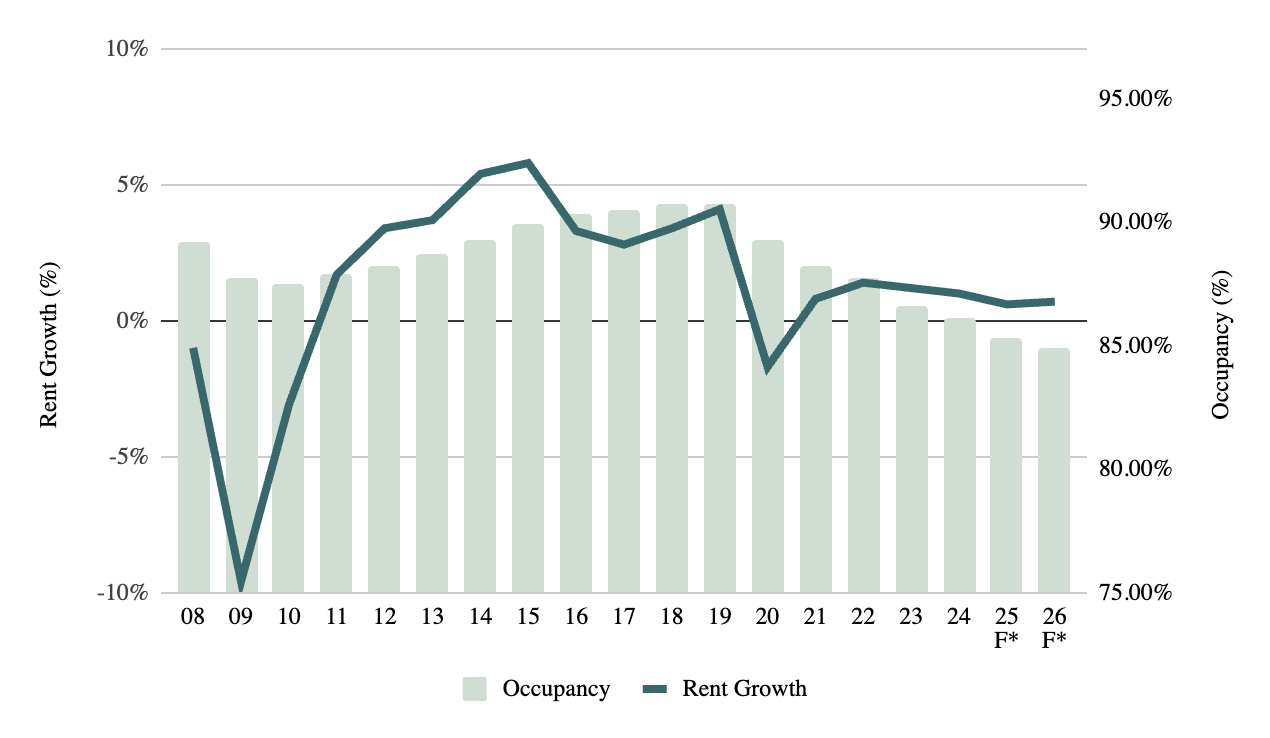

The industrial sector faces some challenges while maintaining pockets of strength - some large warehouses face oversupply while smaller facilities maintain tight occupancy.21,22 E-commerce growth is helping keep demand strong, and stabilizing supply trends and slowing construction are expected to help improve the supply-demand balance by mid-2025.21

Green Street notes that demand has kept industrial properties among the most expensive in CRE.7 However, CoStar reports vacancy rates have climbed steadily for nine quarters, reaching 6.9% in Q4 2024, up from a low of 3.8% in 2022, likely showing that new construction has outpaced demand, particularly in large warehouses and distribution centers.21

Smaller industrial facilities, such as light industrial spaces and micro-fulfillment centers typically crucial for last-mile delivery, have tight availability rates below 4%, according to CoStar.23 With little new construction planned for these facilities per CoStar, they are expected to maintain higher occupancy levels compared to the oversupplied larger warehouse segment.

Despite supply challenges, recent trends generally point to market stabilization. Vacancies rose by just 0.19% in Q3 2024—the smallest increase since 2022, according to CoStar.21 New supply is also slowing, with 76 million square feet delivered in Q3—the lowest level since early 2021 and 54% below Q3 2023.21 Projections indicate continued declines in new construction in the coming quarters.21

With new supply dropping, the national market is expected to improve further. According to NAIOP’s Industrial Space Demand Forecast, the national supply-demand imbalance for industrial facilities should ease by mid-2025 and improve further into 2026, driven by steady demand and reduced construction.24 Per CBRE, oversupplied markets like Dallas, Austin, and Phoenix are seeing strong absorption trends due to high population growth and relatively robust fundamentals, which are expected to continue in 2025.25

Strong demand in the face of stronger supply has led to a moderating but positive rent dynamic.21 While rent growth has slowed from 10% in 2022 to 2.5% as of December 2024, it remains positive.21 Rent growth nationwide is expected to hover around 2% until mid-2025, after which easing supply pressures are projected to drive an uptick, with rent growth expected to climb to approximately 3.8%.21

Figure 6: Industrial Market Fundamentals by Year with Forecast Per CoStar

Source: Industrial, CoStar, December 2024. *F stands for Forecast per CoStar.

Retail Outlook

The retail market is showing record-low vacancy rates, rising rents, and strong demand for grocery-anchored centers and high-traffic properties, despite a slight contraction in 2024.26

Retail market fundamentals have strengthened over the past decade, supported by limited new development, high construction costs, and the demolition of outdated spaces.26 CoStar reports a record-low national vacancy rate of 4.1% in 2024, with just 0.4% of inventory under construction.26 The pandemic also played a role in helping stabilize the sector by hastening the exit of weaker tenants.

Retail rents reached a record $25.76 per square foot in 2024, partly driven by a 30% increase in nominal sales since 2019, according to CoStar.26 CBRE attributes rent growth to persistent space scarcity and shifting tenant demand favoring smaller and well-located properties that remain competitive and relevant to our daily lives.27 Sun Belt markets have outperformed compared to others in the sector thanks to population and income growth, while older retail spaces in the Northeast and Midwest have struggled with stagnant demographics, per CoStar.

The retail sector saw a slight contraction in 2024 as store closures edged out openings for the first time since the pandemic.26 Despite this, necessity-focused retail, such as grocery-anchored centers and build-to-suits, remained in high demand.26 According to CoStar, grocery-anchored properties, priced 100 basis points higher than single-tenant net-lease assets, demonstrated strong income potential.26 Tenant demand from food services, healthcare, and experiential sectors continues to bolster fundamentals, as noted by GlobeSt.28

CBRE projects foot traffic in retail districts will surpass pre-pandemic levels by late 2025, signaling a sustained recovery.29 With low vacancy rates and limited new supply, retail assets are expected to offer stable market fundamentals, particularly in high-growth suburban areas, according to Newmark.30

Figure 7: Retail Market Fundamentals by Year with Forecast Per CoStar

Source: Retail, CoStar, December 2024. *F stands for Forecast per CoStar.

Office Outlook

The office market faces record-high vacancies and sluggish rent growth.31 Demand varies based on the quality and age of the building and its location.

According to CoStar, the U.S. office vacancy rate hit a record high of 13.9% in 2024, sparking concerns for the overall office market.31 A closer look reveals a growing divide in performance.

CBRE data shows that "prime office" buildings—those considered the best in their metro areas and making up only 2% of all office buildings in the U.S.—have seen steady leasing gains since early 2020.32 In contrast, lower-quality office buildings have generally lost more tenants than they've gained.32

While demand for higher-quality office space remains strong, this performance varies across regions. Newmark data highlights that in Central Business Districts (CBDs), office quality remains a key factor for tenant demand, but in suburban markets, tenants are prioritizing value.33

The performance trend also varies by property age. CoStar data shows that although newer buildings (aged 0-3 years) have maintained positive demand post-pandemic, the pace of tenant move-ins has slowed in 2024.31 As a result, availability rates for these buildings have increased to 27%, well above the long-run average of around 15% and up from 21% in early 2023.31 This suggests that leasing in modern buildings has slowed as occupiers hesitate to pay premium rents except in highly sought-after locations.31

JLL34 & CoStar31 highlight that due to space consolidation, many new leases are reportedly 15-20% smaller than their pre-pandemic averages. Pre-built, move-in-ready suites are increasing in demand, especially among smaller tenants, as flexibility becomes a priority amid broad industry uncertainty.31

National office rent growth remains sluggish, with rents largely flat over the past four years.31 CoStar projects rents will grow by less than 1% over the next few years. However, certain markets, such as Las Vegas and Miami, stand out with rent growth approaching 5%, highlighting pockets of strength.31

Figure 8: Office Market Fundamentals by Year with Forecast Per CoStar

Source: Office, CoStar, December 2024. *F stands for Forecast per CoStar.

Hospitality Outlook

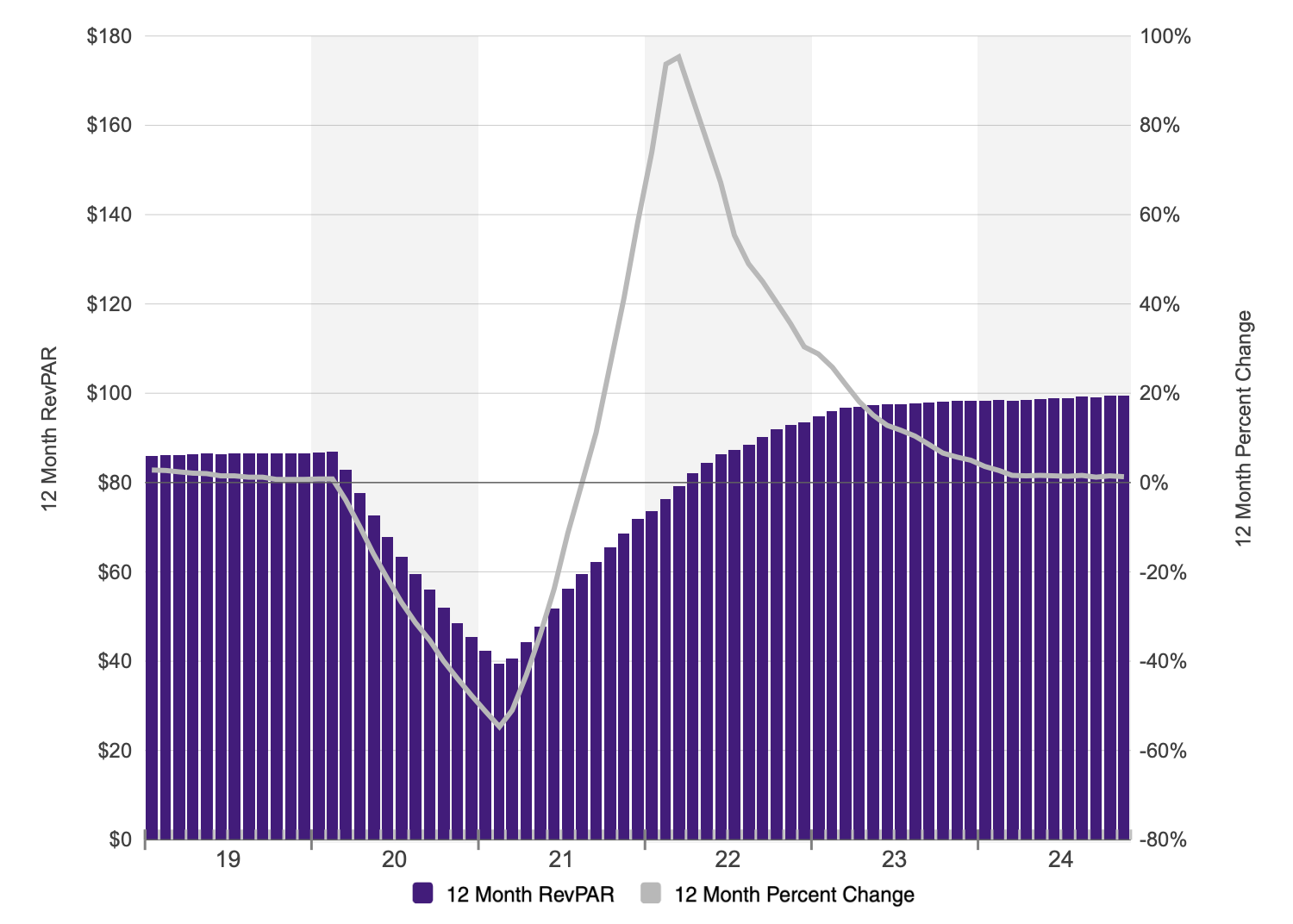

The U.S. hotel industry faces a mixed recovery, with rising revenues driven by higher rates and recovering corporate and international inbound travel but also ongoing challenges from inflation-adjusted revenue shortfalls and uneven market performance.35

According to Smith Travel Research (STR), the U.S. hotel industry’s recovery slowed in 2024.35 Revenue growth was driven by higher average daily rates (ADR), with 12-month revenue per available room up 1.5% and 12-month ADR increasing 1.9%.35 However, 12-month occupancy dipped slightly by 0.4%, reflecting weaker demand (data as of 12/13/24).35 While nominal revenues have returned to pre-pandemic levels, inflation-adjusted figures show the industry has not fully bounced back.35

Operational costs are rising faster than revenue, per CBRE, but STR anticipates lower labor costs in 2025, which could potentially boost profitability.35 Performance varied across markets, with cities like Las Vegas, Houston, Boston, and New York leading the recovery, while San Francisco, Los Angeles, Phoenix, and Orlando struggled.35

According to STR's November 2024 forecast, higher-end hotels, supported mainly by group and corporate travel, are projected to sustain growth into 2025. In contrast, economy hotels will likely face challenges as inflation squeezes lower-income consumers.

According to the U.S. Travel Association, international inbound travel is recovering. Post-COVID hurdles like visa delays, limited flights, and staffing shortages had slowed progress, but visits grew 17% in 2024, reaching 98% of pre-pandemic levels.36 Recovery from Europe and the Americas is leading the way, while travel from Asia lags.36

Figure 9: Hospitality Revenue by Year showing revenue recovery, growth has slowed down.

Source: Hospitality, CoStar, December 2024. RevPAR stands for Revenue per Available Room.