Understanding LP and GP Positions

In the realm of investment partnerships, Limited Partners (LP) and General Partners (GP) play distinct roles. Limited Partners are typically passive investors, providing capital to the partnership. While LPs have the potential to earn returns on their investment, they generally lack decision-making authority on the business plan and day-to-day operations of the investment. On the other hand, General Partners usually take on a more active role in managing the entity responsible for making investment decisions and overseeing the partnership's operations. In addition to the ability to earn potential returns as a result of the capital they contribute to the project, GPs are also often eligible for what is called a 'promote,' which essentially is an added return if certain performance benchmarks are achieved by the investment.

To understand the impact of the GP promote, consider the following example:

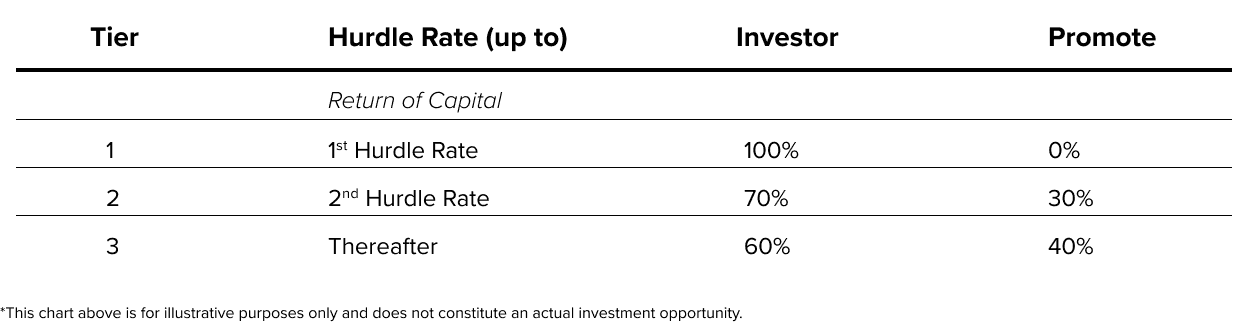

Limited Partners contribute 90% of the equity for this project. The General Partner contributes the remaining 10%. The waterfall is as follows:

How do we understand this?

If the investment has produced returns for investors;

In looking at the Return of Capital line, 100% of distributions go to all investors (including both LP and GP investors) pro-rata until they have received back an amount equal to their initial capital contributions (i.e. their investment amount)

Tier 1: Next, 100% of distributions go to all investors (including both LP and GP investors) pro-rata until the 1st hurdle rate is achieved

Tier 2: Next, 70% of distributions go to all investors (including both LP and GP investors) pro-rata, while the remaining 30% goes to the GP until the LPs achieve the second hurdle rate

Tier 3: Thereafter, 60% of distributions go to all investors (including both LP and GP investors) pro-rata, while the remaining 40% goes to the GP

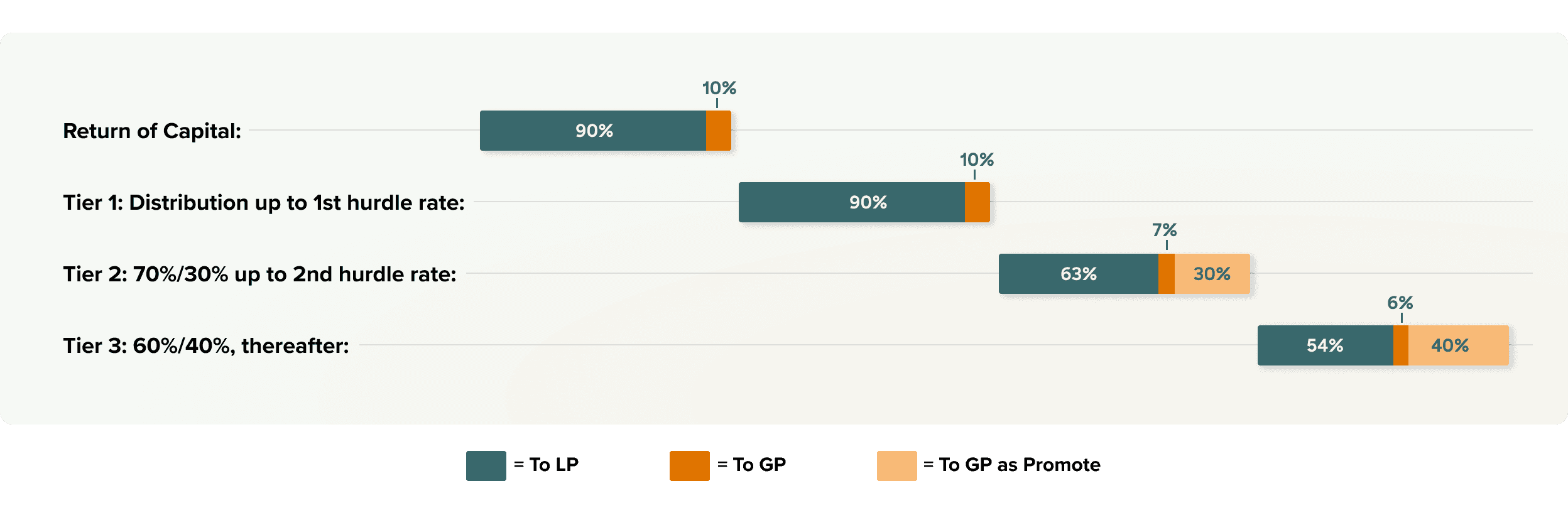

To further illustrate this example, the results of the above would produce the following cash flows:

The above chart is for illustrative purposes only and does not constitute an actual investment. Distributions are never guaranteed.

Due to the GP's 10% equity contribution to the project, a 70%/30% split, as depicted in Tier 2 above, means that the GP participates in their pro-rata share of the 70%, in addition to another 30% of distributions, referred to as the promote. Thus, based on this example, GP investors have the potential to earn a higher return compared to the LP investors if an investment's business plan is executed according to plan. This is made possible through the distribution of profits after specific hurdles are met, at which point the distribution terms are more favorable to the GP given they are earning additional distributions as the promote. However, it is important to remember that distributions are never guaranteed.

How is a GP Fund structured?

Now that you understand the differences between an LP investor and a GP investor, let us introduce the concept of a GP Fund. A GP might offer investors to participate with them as a GP of individual deals and to share in the promote so that its capital can go further. Instead of funding the entire 10% equity position we described above, a GP investor can supplement with investment from others so that the GP's capital can be spread and diversified between more deals. The following is a diagram explaining how a GP Fund could be structured:

How do we understand this?

On the left side of the image above, you see the GP Fund, which is the first layer of the investment. Investors that invest in to the hypothetical GP Fund vehicle will participate as a Limited Partner (LP) in that Fund vehicle, and in the example above, make up 90% of the equity. In this example, the General Partner will contribute the other 10%.

The GP Fund, at the discretion of the Fund manager, will then make several investments into individual real estate projects, as outlined in the Fund governing documents. The GP Fund vehicle will invest as a GP in each of these projects, usually contributing a minority of the equity alongside new LPs associated with each individual project. Each individual project will then have the potential to produce its own promote, as part of the individual deal waterfall we walked through above. If promote is earned, that promote will be paid to the GP Fund vehicle. Note that the GP Fund vehicle may not be the only GP in each of these projects. Instances can occur where the GP Fund invests alongside another GP in the same individual deal, further reducing the Fund's overall investment in the project, in which case any promote in that project would be split pro-rata between the GP Fund vehicle and any other GP investors. Once the promote is divided between the GP Fund vehicle and any other GP investors, the GP Fund vehicle further distributes its share of the promote among its own LP and GP investors, as outlined in the Fund governing documents.