One of the most valuable tools available to investors for evaluating and comprehending risk in direct real estate investments is the 'capital stack'. For the purposes of commercial real estate, the capital stack is the different layers of financing sources that go into funding the purchase and improvement of a real estate project. Ideally, a real estate investment hits its business plan or pro forma target and everybody gets paid according to plan. But, like any investment, real estate has downside risk. The capital stack provides investors with valuable information about where they fall in the pecking order of cash flows, what that order means for risk of repayment and, ultimately, whether the targeted return on investment is worth the assumed risk.

While there is theoretically no limit to the number of layers a capital stacks may contain, we will keep our analysis to the four most commonly used types of capital in ascending order of priority:

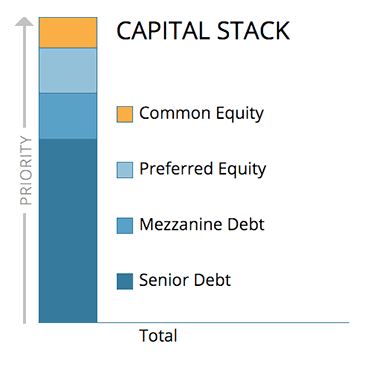

When analyzing the capital stack depicted above, here is the road map for understanding it:

Each capital source has seniority over all capital sources located above it in the capital stack.

Each capital source is subordinate to all capital sources located below it in the capital stack.

Typically, only the senior and junior debt positions are able to secure recorded liens against the underlying asset.

Upon sale or refinance, the bottom position gets paid first until fully repaid and so on.

To the extent that there are insufficient funds to fully repay all capital then losses are incurred from the top down.

This means that risk increases as you move higher in the capital stack.

This also means that returns should increase as you move higher in the capital stack.

Sponsor co-investments are most typically contributed as equity at the highest position in the capital stack.

A good way to think about how capital stacks relate to repayment is to imagine a rectangular prism that is full of water. At purchase, pour the water into a separate container. If things start to go awry, begin removing water from the separate container. If they begin to go better, replace some of the water in the separate container. If things go great, keep adding water to the separate container. Upon sale, pour the water from the separate container back into the rectangular prism. If you fill the entire prism and it begins to spill over, the amount of spillover is your profit! If it exactly refills the rectangular prism, then everyone is repaid but you broke even. If it fails to refill the entire prism then the unfilled portion is your loss and the owners of the unfilled area are the investors in the deal that have incurred the loss.

While the capital stack depicted above has four layers, capital stacks more commonly have fewer layers with the most common being two layers.

For example, think of the financing that goes into buying a home. Typically, a home buyer takes out a mortgage and makes a cash down payment for the balance of the purchase. The mortgage might provide 80% of the total purchase price (the debt portion of the capital stack) while the homeowner contributes the remaining 20% (the equity portion of the capital stack).

Assuming a $400,000 purchase price, that capital stack looks like this:

Fast forward a number of years, and the homeowner now wants to build a new addition. So, she decides to take

out a second mortgage, particularly because the real estate market has been kind to her as the home she purchased for $400,000 just appraised for $500,000. The original lender maintains a first position at the bottom of the stack. The new mortgage slots into the second position and the homeowner is now in third position atop the capital stack with her increased equity (we refer to this increase as 'imputed equity'). Assuming that the first mortgage has experienced $25,000 of amortization since purchase, the new capital stack for that same home now looks like this:

It is important for investors to understand that in a well-constructed capital stack, there is no right or wrong position but, rather, positions that incur more risk or less risk and, in exchange, pay out larger or smaller rewards. By understanding the capital stack, you become empowered to make an informed decision as to where you feel comfortable in the capital stack as well as whether the risk relative to each position is commensurate with the potential reward. For this reason, every offering posted on the Crowd Street platform will include a cleanly articulated capital stack.

As investors grow and diversify their real estate portfolios, it is common to participate in different layers of the capital stack in both debt and equity investment opportunities as a means to spread out risk and generate higher blended returns. The Crowd Street platform offers accredited investors the opportunity to invest at different points in the capital stack such as first position debt, mezzanine financing, and equity investments.

If the junior debt is mezzanine debt then there is typically no recorded lien but, instead, a recorded instrument that grants the mezzanine lender the ability to seize control of the equity entity and remove the equity members.

Learn more about investing in CRE in our updated commercial real estate guide.