If you’ve picked up The Wall Street Journal recently, you’ve probably read that private credit — sometimes called private debt — is one of the fastest-growing asset classes in global finance.^1^

But that’s largely been true for a while. Since the financial crisis, when the category really took hold, the private credit market has grown more than tenfold. ^2^

So why, in the past six months, did Bloomberg call it the talk of the town for anyone within shouting distance of Wall Street? ^3^ Why are BlackRock and Apollo racing to launch ETFs with private credit exposure? ^4^ And why did S&P Global’s 2024 survey rank it the top asset class for future allocation among private market investors? ^5^

There are a few reasons, and we’ll dig into most of them. But a big one is access. Private credit was once primarily the domain of institutions: Investment funds, pensions, endowments. Now, new channels are making it available to individual investors.

That shift has sparked excitement — and questions. The category is still relatively new, and compared to traditional assets like stocks and bonds, its structure and features can feel less intuitive.

This guide breaks it down: What private credit is, some of the opportunities and risks it presents, and how individual investors can invest in one of Wall Street’s most talked-about assets.

What Is Private Credit?

Private credit refers to loans made by funds and finance firms rather than banks. These non-bank lenders operate outside the traditional banking system, providing capital directly to consumers, businesses, or large corporate borrowers. ^6^

Private credit existed before 2008, but it was a niche category, mostly focused on distressed debt. Traditional banks handled the bulk of corporate lending. That began to shift after the Global Financial Crisis, when new regulations pushed banks to scale back on business lending. This opened the door for asset managers to step in.^7^

As banks pulled back, direct lending took off. Asset managers began launching private credit funds to primarily serve middle-market companies. Through these vehicles, they offered more flexible financing, tailored to borrowers who no longer met the stricter standards of traditional banks. ^8^

Graphic courtesy of Cambridge Associates.

Private credit loans often carry floating interest rates and may be secured by real assets or other forms of collateral. Because private credit funds act as lenders, they’re repaid first, entitled to both interest and principal ahead of shareholders. ^9^

For borrowers, these deals can offer financing they might not get from a bank. For investors, there’s potential to earn income from regular interest payments.^24^

While direct lending is the most common form of private credit, the category has expanded. Strategies also include junior debt, mezzanine financing, and distressed lending, among others.

But first, the basics: What are some of the typical opportunities and risks of investing in private credit?

Why Invest in Private Credit?

Private credit advocates often point to three advantages: (1) Potential Income, (2) Reduced Volatility, and (3) Diversification. ^10^

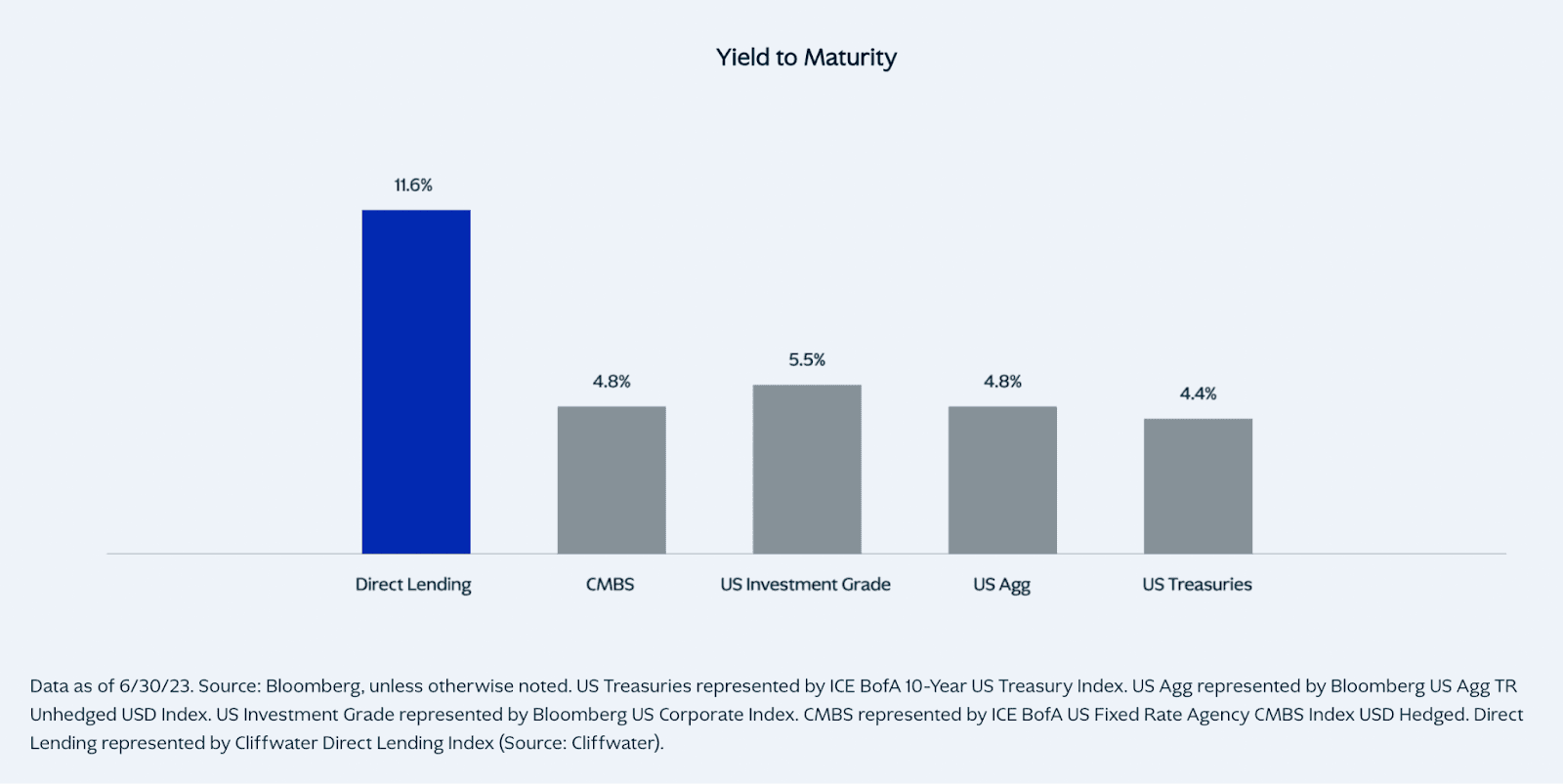

Income: Private credit is structured with the goal of generating income, unlike appreciation-focused investments like venture capital. The objective is for investors to receive payments based on the interest collected from the underlying loans. Yields have historically outpaced those of traditional fixed income assets like bonds, thanks to favorable loan terms, an illiquidity premium, and other factors (graphic below).^11^ That said, the potential for higher returns often comes with higher risks. More on that shortly.

Reduced Volatility: Private credit returns are historically less volatile than equities.^12^ Because these assets aren’t publicly traded, they’re less exposed to daily market swings. And since many loans carry floating interest rates, they offer some protection against interest rate swings — a risk that can hit other asset classes harder. ^25^

Diversification: Private credit has shown lower correlation with public markets than stocks or bonds. For investors with portfolios heavily weighted toward public equities, adding private credit can reduce exposure to market swings^13^ As a note, however, diversification does not guarantee investment returns and does not eliminate risk of loss.

Graphic courtesy of KKR.

Like any investment, private credit comes with its own set of risks. Once again, these risks broadly fall into three categories: (1) Credit, (2) Illiquidity, and (3) Transparency. ^14^

Credit: As with traditional fixed income, private credit carries the risk of borrower default. If a borrower can’t meet the terms of their loan, the fund and its investors can be impacted. This risk can be heightened when a fund is concentrated in a sector facing economic or cyclical pressure, which may affect borrowers’ ability to repay.

Illiquidity: Most private credit investments are illiquid. They’re typically made through closed-end funds or lending vehicles with multi-year lockups, meaning investors can’t quickly access their capital. Some newer fund structures offer limited redemption windows or periodic access, but liquidity remains far more limited than in public markets.

Transparency: Private credit, like other private market strategies, isn’t subject to the same regulatory and disclosure requirements as public fixed income.^15^ That means investors often have less visibility into underlying borrowers and loan performance. Strong due diligence — both by the fund manager and the investor — is essential.

What Types of Private Credit Investments Exist?

The most common form of private credit is senior direct lending: Loans made by non-bank lenders directly to companies, often mid-sized firms. Senior secured debt is often loaned to companies that have been acquired in a leveraged buyout (LBO). ^16^

For this reason, private equity firms play a central role in the private credit ecosystem, as they’re often the acquirers in LBOs. These sponsors typically bring capital discipline, financial oversight, and operational experience — with the goal of using these factors to improve a borrower’s performance and reduce default risk. For lenders, partnering with experienced PE sponsors can add a layer of confidence to underwriting and execution. ^17^

That said, private credit now spans far beyond senior direct lending, involving a wide range of borrowers and strategies. As the market has grown, so has the diversity of approaches it includes.

Each is structured differently, with its own risk. Here's an overview of the most common types: ^18^

Senior Direct Lending: Loans made directly to companies — often middle-market firms — typically secured by collateral and prioritized for repayment ahead of other debt.

Junior Debt: Subordinated loans that rank below senior debt in repayment priority.

Mezzanine Debt: A hybrid of debt and equity, often unsecured and used to fill funding gaps in acquisitions or growth financing.

Distressed Debt: Investments in the debt of companies facing financial trouble or bankruptcy, with the goal of profiting from a turnaround or restructuring.

Specialty Lending: Niche financing strategies focused on specific asset classes or borrower needs, such as litigation finance, equipment lending, or royalties.

How to Invest in Private Credit?

The most common way to invest in private credit is through private credit funds. These funds pool capital from multiple investors to make loans to private companies. Fund managers typically source and bundle deals across various sectors and industries to help limit exposure to any one type of borrower. ^19^

Historically, private credit funds have been dominated by institutions, like pension funds, insurance companies, and family offices. While accredited individuals could invest as limited partners in traditional funds, minimums often start at $5 million, putting most opportunities out of reach. ^20^

Today, the financing needs of middle-market companies exceed what institutions alone can provide ^21^— especially as private equity fundraising slows. ^22^ To fill the gap, companies are seeking new sources of private capital. Firms like Crowd Street are stepping in, offering accredited individuals access to private credit funds with minimums as low as $25,000.

Private credit has the potential to offer compelling opportunities for passive income and portfolio diversification, especially in today’s market. But like any asset class, it comes with risks — from illiquidity to credit and transparency challenges — that investors need to weigh carefully. Doing your homework, understanding the structure of each deal, and aligning investments with your risk tolerance are essential steps before getting started.

When evaluating a fund, investors should look closely at things like the manager’s track record — especially through market cycles — the fund’s underwriting process, borrower selection criteria, loan monitoring procedures, and diversification across sectors and loan types. It’s also worth understanding how the fund handles defaults and workouts, as well as the manager’s alignment with investors, including how they’re compensated. ^23^

For more market insights, visit our Member Resource Center.