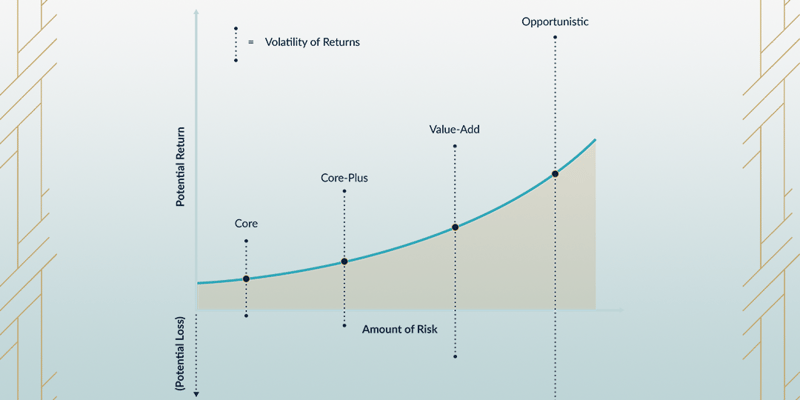

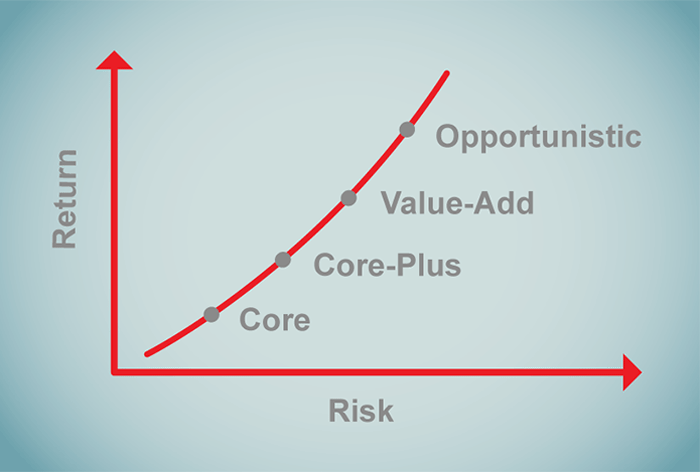

Within private equity real estate, assets are typically grouped into four primary strategy categories based on investment strategy and perceived risk. Those four categories are core, core-plus, value-added and opportunistic. The key differentiator between these categories is the risk and return profile. Moving between those strategies is a bit like stepping up the ladder in terms of taking on more risk, and in theory, being compensated for that risk with a higher return. For this article, we will describe each category and outline the typical level of leverage (see Leverage: The Double-edged Sword of Real Estate Finance) used for each category but also acknowledge that the use of leverage is determined by lenders and borrowers and, therefore, can vary from the ranges discussed below.

Core: Core assets, considered the safest, sit at the bottom of the risk-return ladder. Core properties are relatively stable assets in major metros, such as high-rise office towers or apartment buildings downtown locations in New York City, Chicago, San Francisco, Washington D.C. or L.A. They are usually best-in-class properties in the best locations, with high, stable occupancy and credit tenants. Core assets can be quite large and expensive and, therefore, are usually owned by well-capitalized entities, such as REITs and other institutional investors. Because they are stabilized and already achieve market rents, there is not much value an investor can add, which obviously limits their upside. However, in an economic downturn, they are usually the last to lose tenants. As a result, due to a lack of value-added opportunities that also offer a low-risk profile, core investments usually translate to single-digit annual returns.

Leverage with Core: Can range from 0% to 50% of asset value and rarely higher. The reason for low leverage with core is that it is simply not conducive to the use of much leverage given its low unleveraged returns. Leveraging core assets adds little to leveraged returns so it typically adds more risk than return.

Core-Plus: Core-plus strategy assets occupy the next rung in the risk ladder. Core-plus assets may share many of the same characteristics with core assets with one or more exceptions that create added risk. Some examples of those exceptions might include the age or condition of the asset, a dip in tenant credit or less than stellar location. For example, that Chicago office tower might be two or three blocks off Main & Main, or it might be a historic building rather than new construction. Annualized leveraged returns on these assets generally range from 10% – 14%.

Leverage with Core-Plus: 50% – 65% of asset value. Unleveraged returns on Core-plus assets are high enough to justify the use of leverage to increase leveraged returns. However, leverage is typically limited in order to limit risk and preserve the overall risk-reward balance of a Core-plus profile.

Value-added: Value-added assets take a bigger step out in the risk-reward line. Value-added assets generally have a problem that needs fixing, such as leasing to improve significant vacancy, renovation or re-tenanting to improve the quality of the rent roll. The purchaser is usually coming in with a specific business plan to improve an under-utilized asset. One example is a shopping center that has lost an anchor tenant, such as a grocery store or other big box tenant. The purchaser will have an opportunity to buy that property at a discount given the absence of an anchor. If the new owner has an effective business plan to reposition the anchor space (possibly by demising it into two to three spaces) and bring new tenants to the property that would improve the overall shopping experience, the new owner can make a substantial profit. Just think of what reformatting a former Albertsons into a combination of a Trader Joe’s and a Bed, Bath and Beyond would do for the overall shopping experience and how it would drive traffic to the entire center. A well-executed strategy can turn a value-add asset into a core-plus property. With more risk and effort required to successfully execute the business plan, these investments often provide leveraged returns in the high teens at 15% – 19%

Leverage with Value-added: 65% – 85% of asset value. Unleveraged returns on Value-added assets are now high enough to entice additional use of leverage to further enhance leveraged returns. In addition, re-tenanting and repositioning strategies, as described above, can often be mostly capitalized through additional leverage that is funded by the senior lender post-closing as the business plan is proven out. In industry jargon, we refer to this as “future funding” or “good news money”.

Opportunistic: Opportunistic assets are the final rung at the top of the risk ladder. These deals are generally extreme turnaround situations. There are major problems to overcome, such as major vacancy, structural issues or financial distress. Sometimes referred to as Distressed Assets, Opportunistic strategies may involve acquiring foreclosed assets from banks or servicers or acquiring the senior loan at a discount from banks or servicers with an eye toward eventual foreclosure. Opportunistic investments were plentiful in the wake of the recession as bold investors stepped in to buy properties in distress at a steep discount from previous trades. In some cases, opportunistic deals require special expertise to execute the turn around or patience to wait out a downturn in the market to effect a value-added strategy once tenant demand begins to resurface. Because opportunistic investments carry the highest risk and require the greatest expertise, they can provide annualized leveraged returns of over 20%.

Leverage with Opportunistic: 0% – 70% of asset value. Because of the distressed nature of Opportunistic strategy assets, they are often ineligible for much (and sometimes any) leverage upon acquisition. If you acquired a note, you essentially bought the leveraged part of the deal with a strategy to convert it to a low basis unleveraged asset. The broad range is due to the fact that Opportunistic strategies are highly case dependent. Opportunistic assets may also start with little to no leverage but find their way to leverage or increased leverage as the business plan develops. Think of a situation in which you acquire a 100,000 SF vacant retail building (this is often referred to as a “dark box”) for $3 million or $30/SF all cash that could be worth $18 million or $180/SF with a stable NNN tenant on a long term lease. However, that tenant will require $7 million of tenant improvements and capital improvements in order to entice them to occupy the property. With a signed lease in hand, you could approach a lender, pledge the unleveraged building as collateral and obtain a loan for the entire $7 million needed to perform the work to install the tenant. Once the tenant takes occupancy, you have now a Core-plus asset.

What’s are the takeaways?

It is important for investors to understand the risk and return relationship when discussing the four different types of real estate investment strategies. The level of the return should be commensurate with the amount of risk. Specific to value-add and opportunistic deals, investors also need to keep in mind that the expertise of the sponsor and their ability to create and execute a business plan can be critical to the success of a project.

A well-balanced commercial real estate portfolio may include some or even all of these different investment categories depending on the risk tolerance of the individual investor. The CrowdStreet Marketplace posts offerings across the risk spectrum in each of these categories.