The market is grappling with a perfect storm of:

- Increasing project costs2

- Higher operating expenses3

- Expanding cap rates4

- Rapid rise in interest rates, and

- Diminishing demand for assets leading to declining overall prices at the national level5

At this juncture, CRE as an asset class is adjusting to the new realities that came with changes in U.S. monetary policy, and so is our investment philosophy.

While we believe interest rates may be approaching a short-term peak, no one can accurately predict how long they will remain near their current levels. Because of this inherent uncertainty, CrowdStreet is abiding by the Fed’s “higher for longer” interest rate environment outlook when we contemplate our deal flow.

As we navigate these waters, the following investment characteristics combine to form our North Star:

- Prioritize principal protection

- Capture current lending opportunities associated with high-interest rates

- Move from common equity to preferred equity positions where prudent

- Find projects with the ability to sustainably service their debt

- Place a higher value on what’s present in a deal today over what may be possible down the road

- Seek appropriate discounts relative to peak market values

- Target net yields that exceed the risk-free treasury rate for common equity positions

Entering the next phase of the market cycle we see a high degree of uncertainty as we assess the next 12-18 months. Therefore, we are inclined to generally take a conservative approach on short-term growth assumptions. This approach has three primary implications when we apply it to our current deal flow:

- First, we believe the current high interest rate environment provides a window of opportunity to pursue debt positions. In many scenarios, now may be a better time to be a lender than a borrower.

- Second, we are considering investment alternatives for projects where we have conviction in the quality of the asset, sponsorship, and its business plan but where we lack conviction regarding the project’s ability to deliver sufficient risk-adjusted returns on a common equity position. In such scenarios, it may still be possible to pursue them by adjusting our position in the capital stack from common equity to preferred equity. By doing so, we may potentially take advantage of the current lack of overall liquidity to earn excess yields (both current and accrued) while helping insulate some of our downside by having first dollar loss risk capital in a subordinate position to us.

- Third, given that added uncertainty in the current CRE market environment has increased its inherent inefficiency, we expect to see opportunities to pursue select discounted common equity deals. Particularly, we believe certain assets will be mispriced from an idiosyncratic risk perspective (i.e. risks that are specific to the asset rather than market-based).

Uncertain times can call for creative measures, which means we are looking beyond common equity positions. We are seeking opportunities wherever they seem more viable in the capital stack, assuming they align with our North Star.

.jpg?width=672&height=477&name=Preferred%20Equity%203%20(1).jpg)

Historically, the majority of investments offered on the CrowdStreet Marketplace have been structured as common equity, with a handful of select debt deals presented in cases where they aligned with our thesis

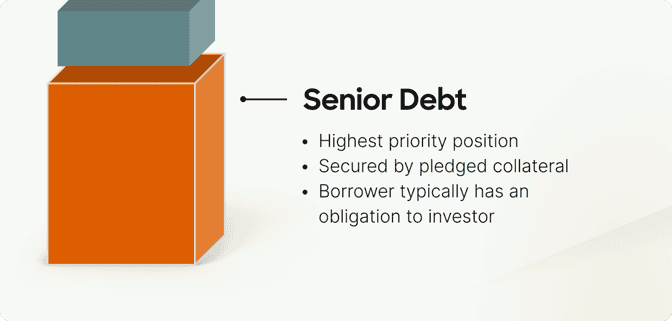

What differentiates an investment into a debt position over other types of investments you may find on the CrowdStreet Marketplace is primarily two-fold:

- The borrower typically has an obligation to make regular interest payments as well as repay your principal at maturity according to a predetermined schedule, and

- Your position is typically secured by pledged collateral (such as a property) and/or may include a guaranty from the borrower to repay the loan.

Investors in debt generally have more rights in comparison to preferred equity or common equity that they are able to use to help enforce upon a borrower in the event of a default. The terms of these loans can vary in structure and their duration can range widely from under one year to ten or more years.

Borrowers typically seek this type of capital for various reasons, which can include acquisition, construction or rehabilitation, refinancing, or as a short-term bridge until they can borrow from a bank. A distinction to remember is that the sponsor in this case would be the lender, and not the operator. When investing in debt, the operator is the borrower.

We believe it is a unique time to be a lender. Seeking debt deals also ties in with our thesis for capital preservation. Preqin reports that private debt gained popularity after the Global Financial Crisis (“GFC”) when banks restricted access to lending and therefore investors used private debt to help fill the gaps in funding. However, while short-term interest rates plunged in the immediate aftermath of the GFC, interest rates today are historically high at the same time that traditional banks have restricted access to lending. This has opened up opportunities for non-bank lenders to enter the market by providing debt capital to those who are seeking to fill in these financial gaps.

We are pursuing debt investing opportunities primarily in two ways:

- Our first strategy is to bring opportunities to invest in real estate debt funds. These are pools of private capital dedicated to investing in loans that are collateralized by real estate and typically spread across a number of assets. Pooling capital in debt funds can help minimize potential concentration of default risk that is typically associated with a single property loan.

- We are also seeking occasional opportunities to invest in single asset-backed loans in situations where we have strong conviction in the asset’s business plan and value of the underlying collateral.

It’s also important to note that we may pursue two different types of debt:

- Senior loans - meaning there is no position in the deal with a higher priority of repayment than the one you are investing in.

- Mezzanine loans - meaning there is a senior loan in the deal that has priority over its repayment than the loan you are investing in. In exchange, you would typically expect a higher interest rate for accepting a subordinated debt position

- Debt investing is typically considered a more conservative approach to real estate investing compared to others because it sits lower in the capital stack compared to equity. You are, by definition, forgoing your upside potential by opting for the higher certainty of interest payments with an obligation for the borrower to repay your principal investment.*

- Many loans offer borrowers the option to repay them prior to their maturity date without penalty. This could mean that you end up with an abbreviated holding period, which can lead to reinvestment risk, especially if future interest rates have declined.

Preferred equity, as the name suggests, is “preferred” over common equity, meaning it has repayment priority over common equity. Deals with preferred equity are typically structured to strike a balance, both in risk and reward, between debt and common equity and in terms of priority of payments. Because debt is a hard obligation, it gets paid first and it must be paid, otherwise the project is at risk of default and potentially subject to foreclosure by the lender. Once debt payments are satisfied, it is typical to see the preferred equity position receive up to its entire prescribed current payment before the equity position receives any payments.**

Preferred equity positions also usually contain a predetermined accrued return that is paid out at exit and often paid in full prior to any payments to the common equity position.* We delve into detail about the characteristics of preferred equity in our article titled, “Preferred Equity 101: The Potential to Hedge the Downside Scenario by Limiting the Upside.”

Considering that there is a heightened level of near-term market uncertainty, we will aim to potentially increase our probability of earning a current cash yield while seeking to add a possible layer of downside protection for certain deals by opting into preferred equity tranches rather than going higher in the capital stack with a common equity position.

We may pursue a preferred equity position when evaluating deals where, although we have conviction in the sponsorship and the quality of the asset, we have a more conservative outlook on its future value.

We’re primarily targeting single asset opportunities that fit our investment thesis and where sponsors are open to entertaining CrowdStreet’s participation in a preferred equity tranche. Additionally, we may also pursue allocations into funds that aggregate portfolios of preferred equity interests.

Finally, because preferred equity can have debt-like characteristics, a key additional benefit is that it can offer more concrete investment time horizons. As a result, we are prioritizing opportunities that include maturity dates (and possibly extension periods) that run co-terminus with the senior debt position.

- You may be forgoing the upside that would be paid to common equity investors in the event the investment outperforms expectations.

- You can still potentially lose 100% of your investment, which is an inherent risk of any equity investment in real estate.

.jpg?quality=low&width=672&height=321&name=Frame%20308%20(6).jpg)

Although common equity investing has historically been our anchor, the current environment has made it more challenging to find deals that make sense in this tranche of the capital stack. Sitting at the very top of the capital stack, common equity investors are the lowest in repayment priority but are generally offered the highest potential returns relative to other investors (e.g. for debt or preferred equity positions). But because of today’s high cost to borrow and service debt, it can be more difficult to have conviction in achieving upside scenarios.

Today, rewarding common equity investors requires accepting additional risks relative to the period prior to 2022 (when the payment hurdles that stood in front of common equity investors were lower).

Despite the current headwinds, there are select opportunities today where we believe projects may be appropriately discounted from their peak prices. CRE prices have declined by 16% on a national level from their March ‘22 peak, which has opened the window for the prospect of aggressively discounted opportunities.1 If interest rates subside in the years ahead, certain discounted properties may bounce back in value and offer potential upside to those investors who shopped the sale.

We are focusing on single asset opportunities with some of the following characteristics:

- Deals where we believe the going-in basis has been discounted enough to potentially counterbalance the effects of high interest rates, backed by an experienced sponsor that is willing and able to offer common equity investors a profit sharing structure that is fit for an illiquid market.

- Discounted opportunities that have assumable debt that is below current market rates (meaning that we are able to take over an existing fixed rate loan that offers a lower interest rate than what is achievable in the current market).

- Un-levered opportunities where we can participate in a deal without the use of debt to help reduce risk in a common equity position by opting out of an expensive debt market. This can also give us an opportunity to consider placing debt on the asset in the future, if and when interest rates subside.

Essentially, we are seeking to bring projects with adequate and sustainable Debt Service Coverage Ratios (“DSCR”). This means that the debt service is adequately covered by the potential current income of the project so that it doesn’t reduce the potential cash flow, now and in the future.

- In most cases, you must pay higher current yields to senior debt and equity positions.

- You sit in the most subordinated and risk heavy position of the capital stack. You accept that one or more tranches of capital are in a priority position to your investment both for current cash flow and potential return of principal.